Bloomington staring at potential $16M deficit by 2029, hoped-for solution in bigger income tax pie

Bloomington could face a growing deficit tied to SEA 1, with reserves potentially strained within three years. A now plausible option under HB 1210—a countywide tax shared across jurisdictions—could yield more revenue even at an 85% share. That depends crucially on the county council.

In the wake of SEA 1, a major revision to the laws governing Indiana’s property tax and income taxes that was enacted in 2025, the city of Bloomington’s financial picture looks grim.

The outlook is still grim even after enactment of this year’s HB 1210, which modifies SEA 1.

A basic sketch of Bloomington’s current landscape was laid out a week ago, on March 13, when the city council’s fiscal committee got a briefing from two financial advisors, Justin Chang and Tim Stricker with Reedy Financial Group.

For the next two years, there’s a roughly $3-million deficit projected for the city’s general fund. The shortfall is due at least in part to the already seen reduced property tax revenues, based on the impact of SEA 1. That’s even though about $7.5 million worth of capital outlays have now been removed from general operating funds, Stricker told the committee.

The four-member group includes Matt Flaherty, Dave Rollo, Isabel Piedmont-Smith, and Hopi Stosberg. Also attending the meeting was city controller Geoff McKim.

The $10.5 million that is projected by Reedy as an annual general fund shortfall (including the capital outlays) is already reflected in the 2025 year-end balance sheet for 2025.

In 2025, the expenditures of about $161.7 million exceeded revenues of about $151.2 million. That reduced the beginning balance of roughly $55.3 million by about $10.5 million to an ending balance of around $44.9 million. No more than about three more years of that pattern would be possible, before the general fund balance would start to look precarious.

But according to Stricker, the basic $3 million deficit, without factoring in the capital expenses that need to be covered, could grow to as much as $9 million a year. That’s after the impact of reduced revenue from a new local income tax scheme is felt, which now starts in 2029, based on HB 1210. That’s a one-year delay compared to the timetable set by SEA 1.

What could help stave off the potential $16 million worth of total annual deficit for Bloomington is a possible choice by the city that is made more plausible by HB 1210—to use what SEA 1 calls a “municipal services” countywide tax rate.

Under SEA 1 alone, residents who live in an unincorporated area of the county were essentially insulated from that extra 1.2 points worth of potential tax that a city can impose. So all other things being equal, a resident of an unincorporated part of the county would pay a maximum of 1.7% local income tax, under SEA 1. Compared to the current total rate of 2.14% which is paid by all residents of Monroe County, that’s a tax break of almost a half a point.

But there’s a feature of HB 1210 that could erase that tax break for residents of the unincorporated parts of Monroe County. That feature is the possibility that a city like Bloomington could opt in for a rate of up to 1.2%, imposed across all county residents, with the revenue distributed to cities and towns with a population-based formula that has been tweaked compared to SEA 1. In the terminology of HB 1210 and SEA 1, this rate of up to 1.2 percent is called the “municipal services” rate.

The big new wrinkle in HB 1210 is the 1.5 multiplier for cities and towns in the distribution formula for the 1.2 percent. Instead of distributing the revenue proportionally based purely on population, HB 1210 calls for the populations of cities and towns to be multiplied by 1.5.

The projected revenue from a 1.2% local income tax rate imposed on all residents of Monroe County in 2029 would be about $57.57 million according to the Reedy Financial Group analysis. And based on the 1.5-multiplier for population, Bloomington would get 85% of that, or $48.9 million. That’s $16 million better than the $32.5 million in revenue the city of Bloomington would see, if it imposed a 1.2% local income tax rate on just its own residents. That would just about cover the $16-million annual deficit analyzed by Reedy.

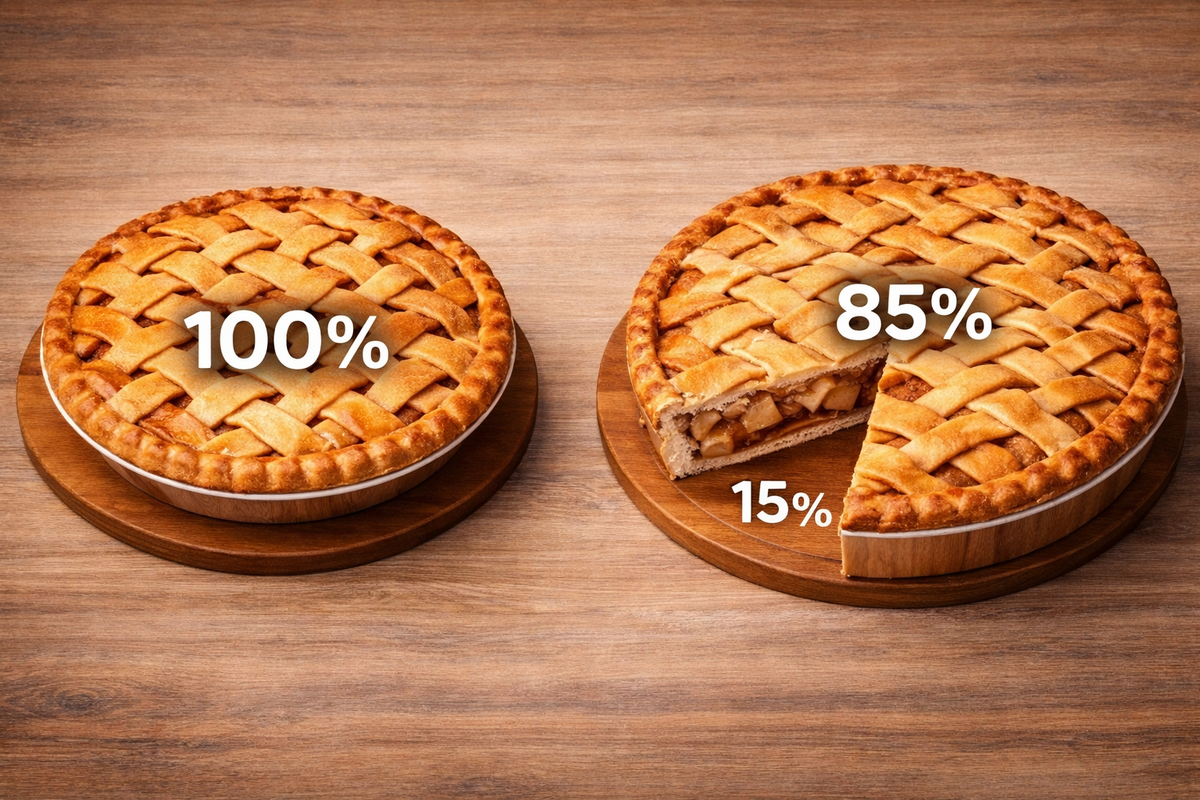

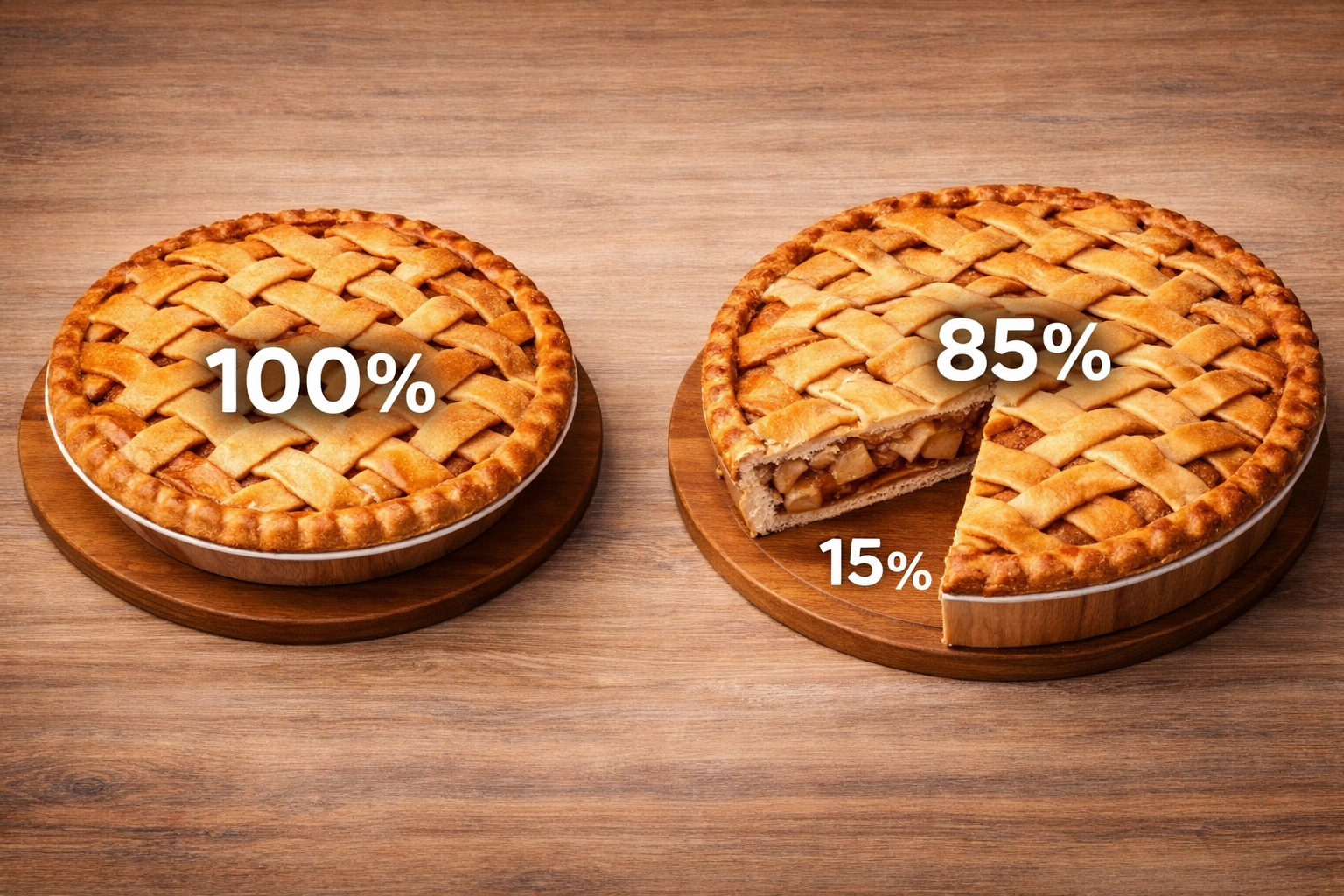

To use a culinary analogy, if the city of Bloomington bakes its own pie, using ingredients just from its own residents, it gets to eat 100% of it. Bloomington also gets to decide the size of the pie tin, which maxes out at a 1.2% rate.

But if Bloomington helps to bake a bigger, collaborative pie, from ingredients collected from all county residents, it gets to eat just 85% of it—but could wind up with way more pie. Still, that depends on the size of the pie that gets baked. The scenario sketched out by Reedy Financial Group assumes that it’s a 1.2% pie tin, or the maximum size, that is baked from countywide ingredients.

But the size of a collaborative pie tin is not up to Bloomington to decide by itself. All other things being equal, the municipal services countywide rate would be set by the county council and it could vary from year to year. There could be an annual political struggle for the city of Bloomington to convince the county council to set the rate high enough, so that the city’s 85% share of the pie would still mean more pie on Bloomington’s plate than it would get from just imposing 1.2% on its own residents.

But that annual political fight could be avoided for a three-year stretch, through collaborative action by the city of Bloomington, the Monroe County council, the town of Ellettsville, and the town of Stinesville. The collaborative action would be taken by the fiscal officers from the towns, and a representative from the county council, who could form what HB 1210 calls a MUST task force. The acronym stands for Municipal Unit Strategic Taskforce.

If the MUST task force reaches unanimous agreement, it could set a rate of up to 1.2% using an agreed upon distribution method that would be in effect for three years starting in 2029. That would give budget predictability and bond market confidence. But the deadline for the unanimous agreement by the MUST task force is Oct. 1, 2026. So the formation of a MUST task force could start to get some air time at public meetings in the near future.

In any scenario except one—where Bloomington sets its own rate (almost certainly the maximum of 1.2%) and imposes it on just Bloomington residents—the county council would be a key decision maker in the setting of rates for local income tax that affect city revenue. Political pressure on county councilors, from residents of the unincorporated portion of the county, would, all other things being equal, tend to push that rate lower.

Reedy Financial Group Handout

These numbers are an excerpt of a table. For the complete table, see the fiscal committee’s meeting information packet for March 13, 2026.

(County Receives Remainder)

(County Wide LIT Opt-In)

Comments ()