Analysis: Refresher for possible local income tax increase in Bloomington, rest of Monroe County

Bloomington mayor John Hamilton’s state of the city address last Thursday included a proposal to increase revenue, but was light on detail.

No amount was provided for a possible local income tax (LIT) increase.

No amount was provided for a possible local income tax (LIT) increase.

But sometime in the next eight months or so, an increase to the current 1.345 percent tax on the incomes of Monroe County residents is likely to get a vote.

In the state of Indiana, local income taxes apply on a county-by-county basis. In counties like Monroe, where a city has a majority of the population, the political power to increase the tax rests mostly with the city.

In 2020, the Bloomington city council’s vote on a quarter-point LIT increase came in mid-September. The timing is affected in part by details of state law. The quarter-point increase was half what Hamilton had floated on New Year’s Day that year, but it failed 4–5 in front the city council.

Because the proposal didn’t have majority support even on the city council, there was no need for the Monroe County council or the Ellettsville town council to consider the proposed increase.

A lot has changed in two years.

One difference this time around is that Hamilton is not leading with a proposed amount for a LIT increase to fund climate action initiatives, with a promise later to identify specific spending proposals for the additional revenue.

This year’s approach could be analyzed as a response to a criticism heard two years ago: The mayor should have first identified the needed programs, next calculated the cost of the programs, then based a request for a LIT increase on the specific costs.

During Thursday’s speech, Hamilton put some effort into establishing the need for more revenue—to fund programs, from basic services, like public safety, to climate action.

What has not changed in two years are some of the basics related to how local income taxes can be increased.

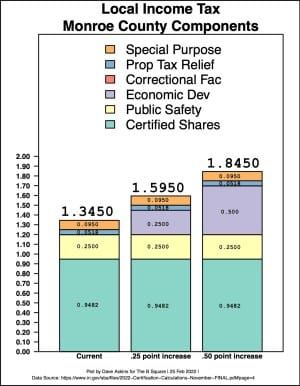

Current rates, describing increases

The current local income tax for Monroe County residents is 1.3450 percent. The biggest part of that rate is made up of two basic components: certified shares (0.9482); and public safety (0.25).

The other 0.1468 is made up of components called “special purpose” and “property tax relief.” The first of those is for juvenile services. The second uses income tax to replace the property tax for homestead properties.

Increasing the rate from 1.3450 percent to 1.8450 percent is a difference of 0.5 percentage points. Sometimes that amount of increase is described as a “0.5-percent increase”—but that’s misleading at best. Strictly speaking, the increase from 1.3450 to 1.8450 is about a 37-percent increase.

The B Square aims to describe the simple arithmetic difference between two rates as the number of “points.” An increase from 1.3450 percent to 1.8450 percent is a half-point increase. An increase from 1.3450 percent to 1.5950 percent is a quarter-point increase.

Categories of LIT

The LIT increase proposal in 2020 was for a category not currently used for the Monroe County tax: economic development.

The economic development category is pretty flexible in the way revenue can be used. There’s a catch-all category in the statute that says a local unit of government can use economic development LIT for “any lawful purpose for which money in any of its other funds may be used.”

That’s likely an argument that will be made for using the economic development category, as opposed to a category that is more restricted in its use, like one specifically designed to fund construction of new jails. The upcoming possible renovation or replacement of the Monroe County jail could come with a price tag in the range of tens of millions of dollars.

The revenue from an economic development LIT increase could be used to pay for a new jail.

Certified shares, the biggest piece of the current LIT rate, are also flexible in their use.

The difference between increasing the certified shares rate and adding a new economic development rate includes the answer to this question: Which governmental units get a share of the revenue?

An economic development LIT increase would be split among Bloomington, Monroe County government, Ellettsville and Stinesville.

An increase to the certified shares rate would be split out not just to those four entities, but also to all the individual townships, Bloomington Transit, the Monroe Fire Protection District, and the Monroe County Public Library.

Limitations on econ dev LIT revenue?

Even if revenue from the economic development category of LIT can be spent on almost anything, it’s not a free-for-all.

Under Indiana state law, expenditures made using economic development LIT revenue are supposed to follow a capital improvement plan. If this year’s proposed increase in LIT is for the economic development category, then a lot of the political action could come in the form of debate on the components of the required capital improvement plan.

In 2020, Bloomington’s city council approved the creation of a sustainable development fund advisory commission (SDFAC), to help provide some extra local oversight for expenditures made using the additional revenue from the LIT increase.

Even though the commission was created, the city council rescinded its action, immediately after the LIT increase failed on a 4–5 vote.

Under the ordinance creating the SDFAC, a new non-reverting fund was to have been created for the additional LIT revenue, called the sustainable development fund. Membership on the SDFAC would have consisted of: the mayor, three councilmembers and three citizens.

Creating such a commission was at least in part an effort to overcome political opposition to the LIT increase. Whether a new commission is proposed this time around could be taken as a measure of how much political opposition to the LIT increase is perceived to exist.

How does voting work for LIT increases?

In Monroe County, any LIT increase has to be approved by the local income tax council—which includes as voting members, Bloomington’s nine-member city council, Monroe County’s seven-member county council, and Ellettsville’s five-member town council.

The 100 total votes available are allocated in a way that is related to population.

For the city of Bloomington and Ellettsville, the votes are allocated based on relative population in the county. For Monroe County government, it’s not the relative portion of the population (which would be 100 percent), but rather whatever is leftover after Bloomington and Ellettsville’s shares are subtracted.

Bloomington’s share of the county’s population dropped from 58.3 to 56.7 percent between the 2010 and the 2020 census.

That kind of change would have certainly not made any difference before 2020, when the votes of each government body were treated as a bloc. This is, before state law was changed in 2020, all of Bloomington’s 58 votes would be cast in favor or against any proposed LIT increase. That meant that a mere five-vote majority of councilmembers could impose a local income tax countywide.

After the state law was changed, in time for the 2020 city council vote, the percentage of votes is now allocated to individual members of the relevant bodies.

Now, each individual member of a governing body is allocated a proportionate share of the group’s allocation of votes. To compute an individual Bloomington city councilmember’s share of the 100 votes, it’s a matter of multiplying one-ninth by Bloomington’s fraction of the Monroe County population under the 2020 census [1/9*(79,168/139,718)*100]. That’s 6.30 votes, rounded to the nearest hundredth.

Eight city council members still have enough voting power to enact a countywide LIT increase [6.30*8 = 50.4]. But the votes of seven Bloomington city councilmembers are not enough. If only seven Bloomington city councilmembers voted in favor of a LIT increase, then additional support would need to come from a member of the county council or the Ellettsville town council.

It’s the same situation as in 2020, before the census numbers had been reported. That is, the political power of the Bloomington city council on the topic of LIT has not decreased, due to the population decrease.

How much money would a LIT increase generate?

The current public safety local income tax rate is 0.25 percent. So the total amount of revenue generated by the public safety LIT can be used as a measure for the amount of increased revenue that a quarter-point increase would yield.

Based on the state’s certified local income tax distributions for 2022, a quarter-point increase would generate a total of $9,025,682 a year countywide.

Based on property tax footprint, Bloomington would see about $4.62 million a year of the $9.03 million total.

Under the economic development category of local income tax, there are two different options for distributing the revenue. One is based on a property tax footprint. The other is based on population. Using a population-based approach would give Bloomington about 56 percent of the revenue. Using the property tax footprint would give Bloomington a little less than that.

Political considerations would probably point to Bloomington proposing the property tax footprint as the basis for the distribution.

Comments ()